Trading is not just about making profits, but also about minimizing risk. A good Forex trader should be able to maximize returns, while keeping the risk to a minimum. The question is how to know the level of risk taken for generating a particular amount of profit? This article looks at the commonly used measures for the assessment of risk-adjusted return in Forex trading.

Net Profit vs. Absolute Drawdown

Absolute drawdown is the largest loss taken below the initial trading capital.

Absolute drawdown = Initial trading capital – Lowest trading capital

For example, let's assume the initial trading capital of $10,000.

Lowest trading account balance below the initial capital = $6,000 (after a series of losses).

Absolute drawdown = $10,000 – $6,000 = $4,000.

If your total net profit during the period of that streak of losses was $1,000 (i.e., you recovered from $6,000 to $11,000), your risk-adjusted return based on the absolute drawdown is $1,000 / $4,000 = 0.25. Obviously, the higher is the ratio, the better.

Net Profit vs. Maximal Drawdown

Maximal drawdown is the largest erosion in the value of a trading account before a new high is established.

Maximal drawdown = Peak value before the largest decline – Lowest value before the establishment of a new high

For example, let's consider that a Forex trading account started with an initial capital of $10,000, increased in value to $13,000, then decreased to $9,000, and then increased again to $12,000, then decreased to $8,000, and finally increased to $14,000.

Maximal drawdown = $13,000 – $8,000 = $5,000.

In this example, the final net profit is $4,000 and the risk-adjusted return based on the maximal drawdown is $4,000 / $5,000 = 0.8. As with the absolute drawdown, the higher is the ratio of profit vs. drawdown, the less risky is the total gain.

Relative Drawdown

Relative drawdown is the ratio between the maximal drawdown and the corresponding high value of the equity:

Relative drawdown = (Lowest balance value - Highest equity value) / Highest equity value * 100%

For example, if an open position results in an increase in the equity value of a trading account to $15,000, before falling to $8,000, then the relative draw down is calculated as follows:

Relative drawdown = ($8,000 - $15,000) / $15,000 * 100% = 46.6%.

In this example, if the trade is closed at a loss of $2,000, then the absolute drawdown is only $2,0000, while the maximum drawdown is $7,000.

Sharpe Ratio

Sharpe ratio is one of the most popular tools used by investors and fund managers to calculate the risk-adjusted return in stocks. It is less popular among Forex traders because it values low volatility of returns even if it is positive. Sharpe ratio is otherwise referred to as reward-to-variability ratio. It is the average return earned in excess of the risk-free rate per unit of volatility.

where:

- RFR is the risk-free rate, which is normally assumed as 0% in Forex trading.

- SD is the standard deviation.

- AHPR is the average holding period return on investment or, simply put, an arithmetic mean of a relative gain per trade.

In general, the higher the Sharpe ratio, the more risk-efficient is the trading system and the smoother is its return over time.

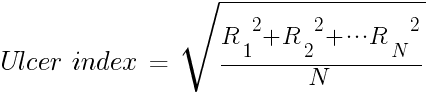

Ulcer Index

Ulcer index a risk-adjusted return measure that calculates the average relative drawdown after each trade. To calculate the Ulcer index, you first find the relative drawdown for each trade that results in a balance lower than the maximum balance so far:

Then, the quadratic mean of the drawdowns for all the trades is calculated:

The lower the index is, the better (less risky) is the strategy. Ulcer index is more suitable for measuring the risk-adjusted returns in retail currency trading compared to Sharpe ratio because it will not deteriorate during a sudden high-profit trade.

The above ratios enable a trader to calculate the risk-adjusted return of a trading system. However, a trader should avoid curve fitting to accomplish theoretically perfect ratios. As long as the ratios do not paint an extreme picture, the trader can concentrate on market analysis.