Average True Range

The idea of average true range (ATR) was devised by Wells Wilder in his ground-breaking book, New Concepts in Technical Trading Systems, in 1978. ATR is not used much as an indicator but is useful as a reality check in setting stops and targets.

Range refers to the high-low range of a bar of any timeframe — hourly, H4, daily, whatever. Wilder named it “true” range instead of plain old “range” to account for gaps. Because the Forex market is nearly 24 hours per day, we get daily gaps mostly on Sundays when Asia is the first session to open up after Friday’s New York close, although we do sometimes get gaps on other occasions (such as central banks’ releases and important data releases like US payrolls). We also get gaps on timeframes shorter than one day. Actually, we get gaps on all timeframes, but they are noticeable only on lower timeframes.

You can read more about gaps in the lesson on Bar Charts.

If you do not have a methodology to account for gaps and you have two periods in a row with the exact same high-low range in terms of the number of points, you will miss that in between the two bars, something important happened. Gaps are not accidents. Gaps appear because a new piece of information has arrived on the scene that causes sentiment to jump, literally. If you were willing to buy EUR/USD at 1.3500 but are waiting for 1.3490, and new wildly pro-euro data comes out, you will change your bid to 1.3525. The very existence of the gap informs other traders that something big has happened. Not every gap sets off a bandwagon, of course, but a new wave of buying or selling ensues from a gap more than half the time. Remember that it may not be long-lasting, though.

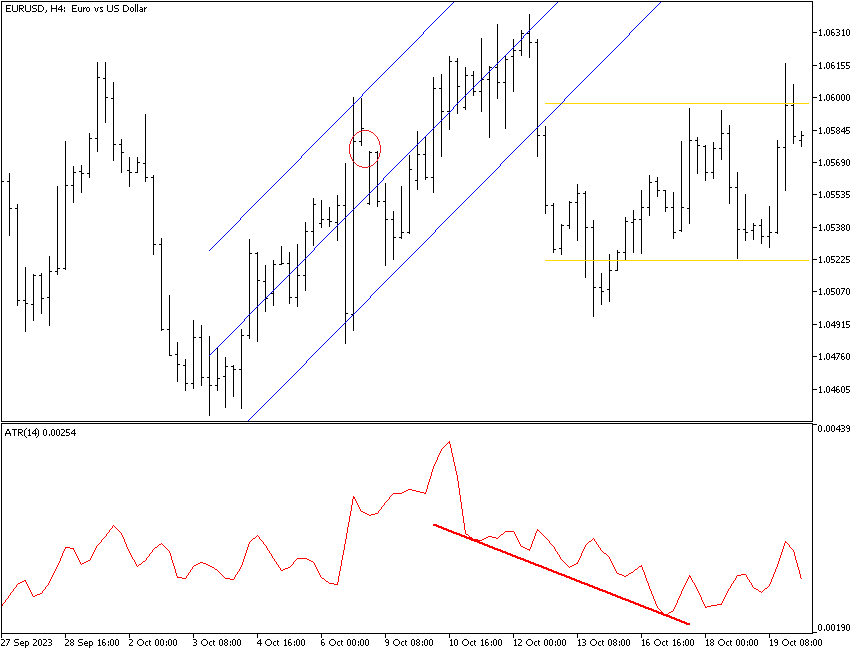

Before getting into the arithmetic of ATR, consider the ATR as an indicator. The chart below shows a 14-period ATR after the uptrend in the price falters. The ATR starts falling and keeps falling even after the price stops falling and recovers a little. The falling ATR is a warning that the currency is in a sideways trading range, marked by gold horizontal lines. The point: falling ATR values mean the market is indecisive and non-trending. When EUR/USD is trending, that 14-period ATR is about 42 points. After the breakout to the downside, it falls to about 22. Notice that there is a downside gap right after the highest high fails. The price has to surpass that previous highest high and “close the gap” before we can assume the uptrend is resuming. Near the right-hand side of the chart, ATR is rising again, showing more action in this currency, but rising ATR alone is not a reason to buy — yet.

Here is a warning — the ATR line does not follow other trendlines. On the chart above, you can see a standard error (linear regression) channel that points upward, while the ATR line is sideways and choppy. You can also have a lovely uptrend with a persistently falling downward-sloping ATR line or vice versa. Do not use the ATR line to define price trendedness! Nevertheless, it may be useful, especially in conjunction with other indicators, to confirm a lack of directional conviction, as it does in this example.

Wilder’s Average Directional Movement indicator (ADX) uses ATR in the formula to incorporate the range concept. Displaying ATR alone is just a more direct way to estimate the degree of market participation in a move. A big ATR number means lots of trading is going on. A falling or low number means participation is low, and low participation usually precedes a breakout, although it does not tell you in which direction.

Calculating ATR

Most or all charting software offers ATR as a standard feature, so you do not need to calculate it yourself, but it is important to grasp the concept. If you take the high-low range of a currency over 5 periods and just average the numbers, you would get a number that does not represent the actual range if there was a gap. When you had a gap between yesterday’s close and today’s open, you measure from yesterday’s close to today’s high instead of the low, as usual. This makes today’s high-low range a bigger number and, even after averaging, has the effect of widening the range and giving you a more accurate picture of market sentiment — remember, a wider range means more trading activity.

Using ATR

As noted, ATR is not much used as an indicator. ATR is a measure of volatility, with small numbers implying low activity and high numbers indicating plenty of activity. Low volatility precedes a breakout, but we have a visually more compelling indicator to help us measure that — contracting Bollinger bands (what John Bollinger named “the Squeeze”).