Date : 27th October 2022.

Market Update – October 27 – USD Lower, BOC Surprise, META & Samsung Miss.

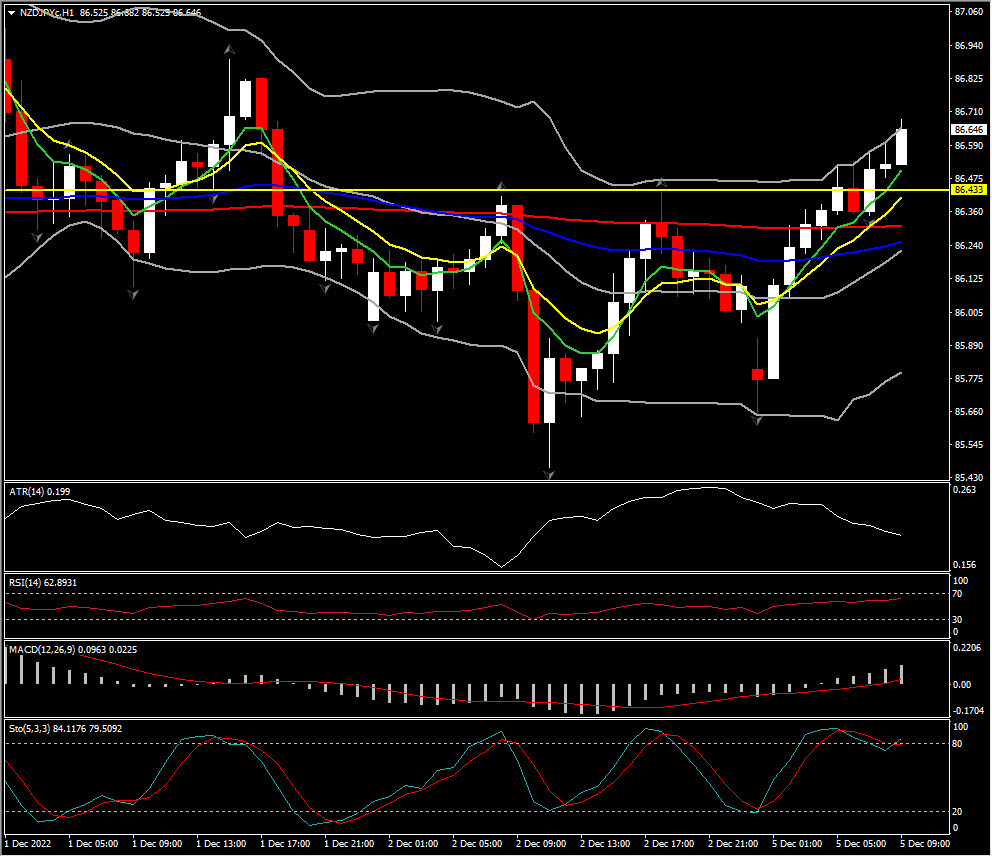

Biggest FX Mover @ (06:30 GMT) GBPJPY (-0.71%) Tank from over 170.00 yesterday to 168.80 now. MAs aligned lower, MACD histogram & signal line negative & falling, RSI 28.05, OS but still falling, H1 ATR 0.299, Daily ATR 2.762.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

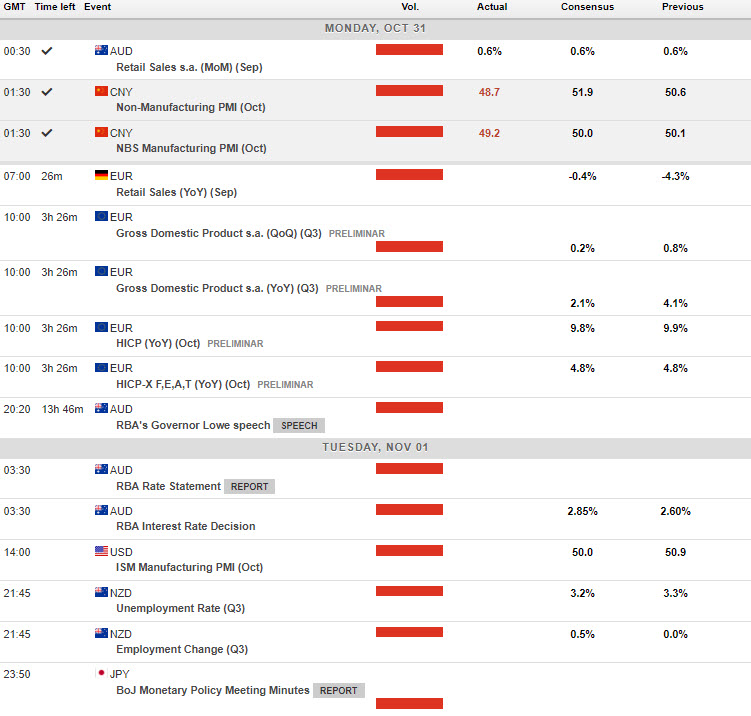

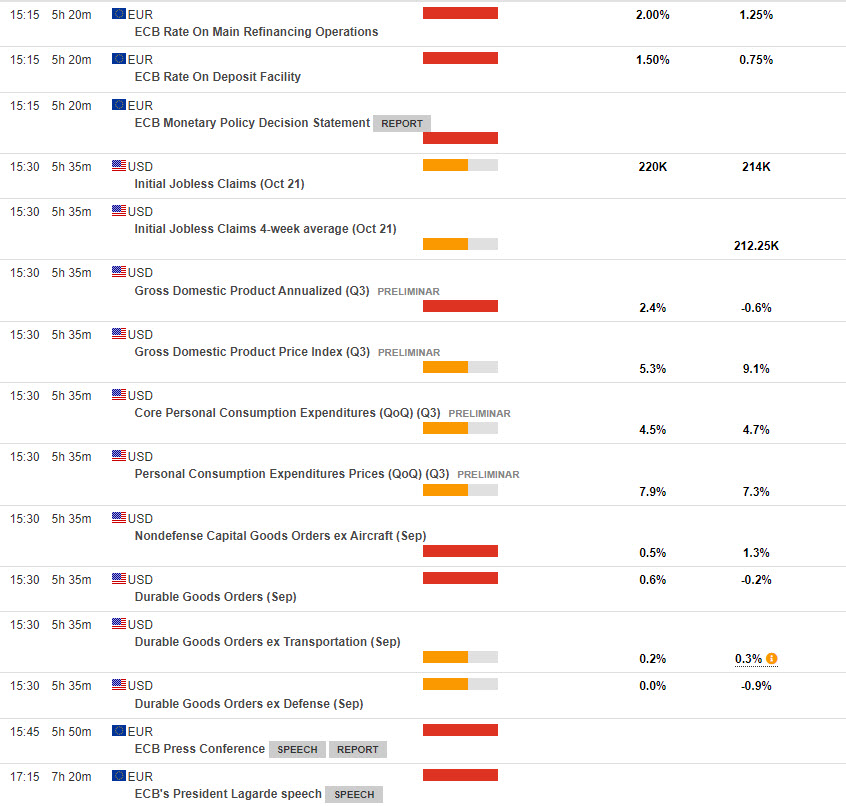

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Stuart Cowell

Head Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – October 27 – USD Lower, BOC Surprise, META & Samsung Miss.

- USDIndex – Slumped to under 110.00 to 109.40. US new home sales dropped -10.9% in September, in line with expectations and BOC surprised markets with only a 50bp interest rate hike to 3.75%. Macklem had suggested more concern over risks from higher inflation following the rise in the latest CPI data. However, it will continue to tighten, sees terminal rate at 4.5%, there is still “excess demand,” in the economy and that a technical recession is just as likely as modest growth, cutting 2022 growth forecast to 3.3% from 3.5%, 2023 to 0.9% from 1.8%, and 2% in 2024 from 2.4%.

- Stocks sank (NASDAQ +2.25%) underperformed. Poor earnings and guidance from big tech (Google plunged -9%), and then Meta (-5.6%) missed and sank -20% after hours, wiping $67 billion off its market cap. Concerns over Apple and Amazon today. Asian markets rose initially but closed mixed. (Nikkei –0.32%, Hang Seng 1.60%), European FUTS also mixed. AUD imports prices 3 x higher than expected, but German GfK Consumer Climate not as bad as expected.

- EUR – leaped over parity 1.0000, land topped at 1.0093 earlier, now ahead of the ECB at 12:15 GMT.

- JPY – Cooled again, under 146.00 to 145.40 lows, ahead of the BOJ rate announcement later tomorrow. Friday’s pre-BOJ intervention peak took the pair to 152.00.

- GBP – Sterling rallied again (another 150+ pips) yesterday to test 1.1600 and trades to 1.1645 today. UK’s mid-term Fiscal statement was postponed from Monday to Nov. 17 as Gilts continue to recover with tax rises and spending cuts expected.

- Stocks – Wall Street were mixed with big moves for Tech stocks in particular. US500 closed -28.5 (-0.74%) at 3830, FUTS trades at 3850 now.

- USOil – rallied from $84.35 lows again yesterday to test $88.40 after inventories showed draw downs, back to $87.60 now. IEA Oil Inventories – big build 2.588M vs 1.029M.

- Gold – weaker USD helped a rally to $1675, yesterday before moving back to $1662 now.

- BTC – rallied again to test $21.0k, back to $20.7k now and holding the important $20k.

Biggest FX Mover @ (06:30 GMT) GBPJPY (-0.71%) Tank from over 170.00 yesterday to 168.80 now. MAs aligned lower, MACD histogram & signal line negative & falling, RSI 28.05, OS but still falling, H1 ATR 0.299, Daily ATR 2.762.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Stuart Cowell

Head Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.