Date : 10th April 2023.

Market Update – April 10 – USD Recovers, JPY awaits Ueda.

US Payrolls on Friday were a near bullseye, with a 236k rise in March after -17k in revisions, though there was a skewing of weakness toward the goods sector. We saw the expected 0.3% hourly earnings rise that left a 4.2% y/y gain. The jobless rate fell to 3.50% from 3.57%, leaving the rate still above the 54-year low of 3.43% in January, with hefty gains of 577k for civilian employment and 480k for the labour force, while the labour force participation rate rose to a new a 3-year high of 62.6% from a prior high of 62.5%. However, there was a further drop in the workweek to 34.4 in March that fueled a -0.1% drop in the hours-worked index after small downward revisions. Overall, it raises expectations of a 25 bp hike from the Fed on May 3rd.

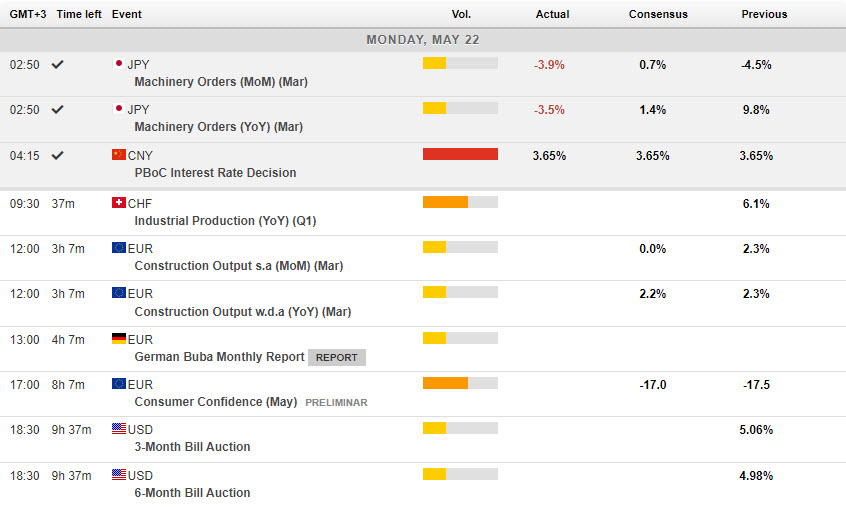

Overnight: Japan – March consumer confidence index 33.9 vs 31.1 prior

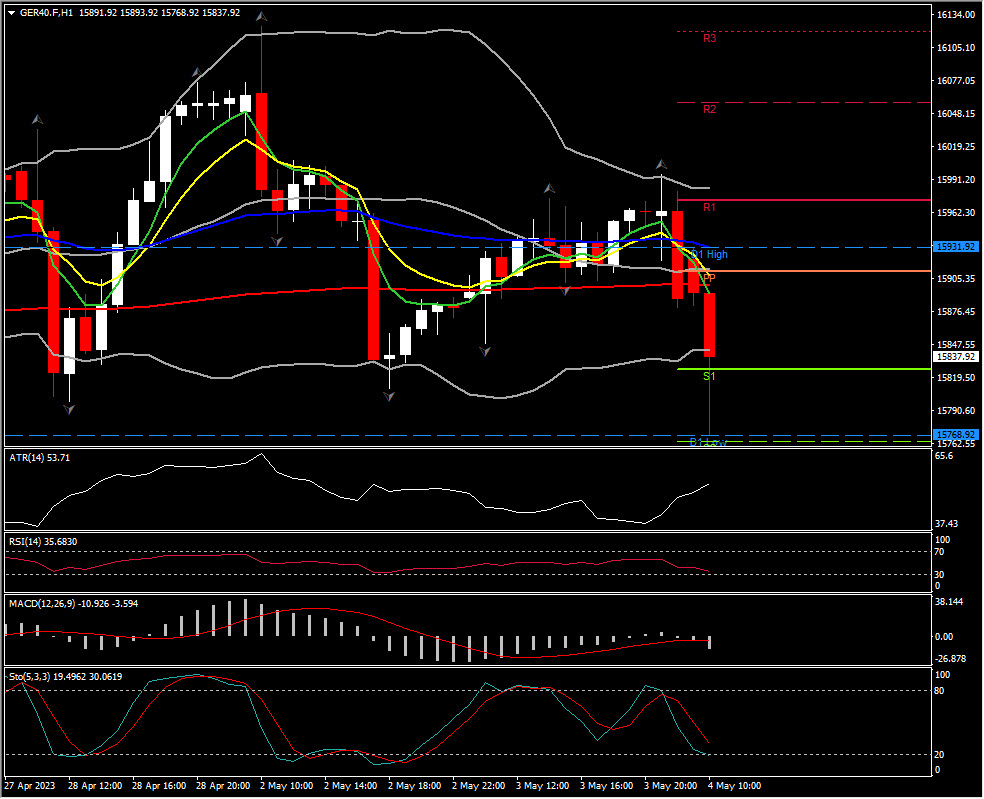

Biggest FX Mover @ (07:30 GMT) USDJPY (+0.49%). A 3-day rally from under 131.00 continues testing 132.75 resistance today. MAs aligned higher, MACD histogram & signal line positive & rising, RSI 62.00 & rising, H1 ATR 0.191, Daily ATR 1.310.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Stuart Cowell

Head Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.

Market Update – April 10 – USD Recovers, JPY awaits Ueda.

US Payrolls on Friday were a near bullseye, with a 236k rise in March after -17k in revisions, though there was a skewing of weakness toward the goods sector. We saw the expected 0.3% hourly earnings rise that left a 4.2% y/y gain. The jobless rate fell to 3.50% from 3.57%, leaving the rate still above the 54-year low of 3.43% in January, with hefty gains of 577k for civilian employment and 480k for the labour force, while the labour force participation rate rose to a new a 3-year high of 62.6% from a prior high of 62.5%. However, there was a further drop in the workweek to 34.4 in March that fueled a -0.1% drop in the hours-worked index after small downward revisions. Overall, it raises expectations of a 25 bp hike from the Fed on May 3rd.

Overnight: Japan – March consumer confidence index 33.9 vs 31.1 prior

- FX – USDIndex slipped under 101.50 on Friday and remains below 102.00 today at 101.85. EUR remains at 1.0900 today, having spiked down to 1.0875 on the NFP data. JPY breached 132.00 on Friday and holds 132.60 ahead of Gov. Ueda. Sterling’s decline from the key 1.2500 tests 1.2400 today.

- Stocks – US markets, closed mixed led by tech stocks on Thursday (+0.76% to -0.03%) #US500 closed at 4105 – US500 FUTS touched 4145 on Friday but are lower today at 4127. Q1 Earnings Season kicks off with the big Wall Street Banks this week.

- Commodities – USOil – Futures hold the key $80.00 and even breached $81.00 briefly earlier following the OPEC production cut last weekend. Gold – broke below the vital $2000, testing into support at $1987, before recovering to $1995.

- Cryptocurrencies – BTC slipped to $27.7k, recovered the key $28k and tests $28.4k today.

Biggest FX Mover @ (07:30 GMT) USDJPY (+0.49%). A 3-day rally from under 131.00 continues testing 132.75 resistance today. MAs aligned higher, MACD histogram & signal line positive & rising, RSI 62.00 & rising, H1 ATR 0.191, Daily ATR 1.310.

Always trade with strict risk management. Your capital is the single most important aspect of your trading business.

Please note that times displayed based on local time zone and are from time of writing this report.

Click HERE to access the full HFM Economic calendar.

Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding on how markets work. Click HERE to register for FREE!

Click HERE to READ more Market news.

Stuart Cowell

Head Market Analyst

HFMarkets

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in FX and CFDs products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.