Arbitrage is a practice of earning money by simultaneously buying and selling the same asset on different markets without exposing yourself to the asset value risk. The simplest example of FX arbitrage would be to buy a currency at one broker at an Ask price that is lower than the Bid price you can sell it at another broker. There are four basic types of arbitrage in Forex:

- Plain currency pair arbitrage between two brokers.

- Arbitrage at one broker involving three or more currency pairs.

- Interest rate arbitrage with a

swap-free broker and a normal broker. - Triangular (or more complex) swap arbitrage at one broker.

Despite their similarity, all these methods are quite different and have distinct advantages and disadvantages.

Currency pair arbitrage with two brokers

Consider this example: the quotes for EUR/USD read 1.0924/1.0925 at a Broker A and 1.0927/1.0928 at Broker B. Obviously, buying EUR/USD at Broker A for 1.0925 and selling it for 1.0927 at Broker B looks like a

2 pips (gain at Broker B) — 1 pip (spread at Broker A) = 1 pip

Advantages

- Simplicity — easy to understand and to calculate.

- Lack of asset value risks — once the right opportunity is detected and the trades are executed, you do not depend on currency rates as the combined position is

market-neutral with zero exposure.

Disadvantages

- The opportunities are rare — the difference in quotes should be sufficiently big to cover the spread and to provide profit.

- You need to have enough margin in two trading accounts to execute the deals.

- You need some technical means of executing both trades simultaneously at two different brokers. It also has to be done two times per one arbitrage operation — for entry and for exit.

- Execution risk is very high due to the

above-mentioned factors. - Transaction costs for transferring funds from a "winning" account to a "losing" account can destroy all the profit.

Arbitrage at one broker with 3+ currency pairs

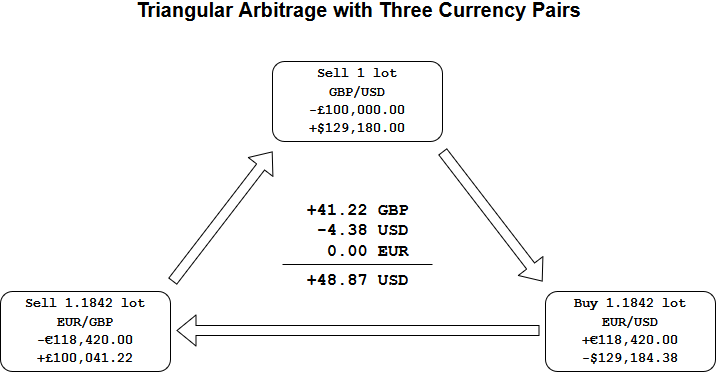

Consider the following example: GBP/USD is trading at 1.2918/1.2919, EUR/USD at 1.0908/1.0909, and EUR/GBP at 0.8448/0.8449.

You buy EUR/USD at 1.0909 and sell GBP/USD at 1.2918. What you get is the locked position, which equals a EUR/GBP Buy at 0.8448 (EUR/USD Ask divided by GBP/USD Bid).

If you simultaneously sell EUR/GBP at 0.8448, you lock 3.2 pips of profit when the rates normalize.

While 3.2 pips might sound quite cool, the problem is that you have to deduct 3 pips of spreads for closing these three positions if you want to realize your profit. That leaves you with 0.2 pips profit, which is still quite good considering its "

What is important to remember here is that you have to use properly calculated position sizes in such triangular arbitrage. In the example above, if you sell 1 lot of GBP/USD, you need to buy 1.1842 lots of EUR/USD and sell 1.1842 lots of EUR/GBP (calculated as GBP/USD Bid divided by EUR/USD Ask).

Advantages

- If everything is executed properly, there will be no exposure to currency risks.

- All money is at one broker — there is no need to transfer cash from the broker where you "win" to the broker where you "lose", unlike in the case of the previous arbitrage technique.

Disadvantages

- Extremely rare opportunities — brokers are not stupid and check their quotes thoroughly. They also might have clauses in their Terms and Conditions prohibiting such arbitrage methods. Still, you might be able to find ECN brokers that would not mind this strategy.

- Involves paying spreads for three positions, which is always costly, and means that the opportunities are next to nonexistent.

- Position sizing calculation is not only difficult but affects the end results as not many brokers let you use precise trade volumes down to a unit. If you are trading on MT4 or MT5, using a cent account is essential to reach the necessary precision.

- Execution risk, although lower than when you have to use different brokers, is still here. Getting a requote or slippage with a triangular arbitrage trade can be deadly.

- Triple margin — you will not get reduced margin requirements due to hedged positions because they are hedged indirectly, so you would need to keep quite a lot of money to pull such trades.

Arbitrage between a swap-free and a normal broker

If you are a savvy trader and are

Consider an example: as of May 8, 2021, you can buy 1 lot of TRY/JPY at one broker and get 0.27 pip daily swap (which is about $2.45) and simultaneously sell TRY/JPY at a

Advantages

- Opportunities are very easy to find — there are many currency pairs with high positive swaps and there is abundance of

swap-free brokers. - No need for any sophisticated execution technology — the swaps arbitrage trades can be found and executed manually.

Disadvantages

- The Bid/Ask spread is the biggest disadvantage of this arbitrage method. First, the spread for currency pairs (exotic ones) that offer such huge swaps are usually very wide. Second, you have to recover both spreads — for your Buy and your Sell — to start earning money. In the example above, if the spread is 40 pips (which can be considered normal for TRY/JPY) at each broker, you will spend 149 days just waiting for the rollover rates difference to compensate the spreads.

- While currency rate risk seems removed here (same as with the first type of arbitrage), the rate movements can be very strong with the kind of currency pairs involved in this. Keeping enough margin to prevent

stop-out might prove difficult. - Brokers hate this. Not the normal

swap-paying ones but the others —swap-free ones. If they find out that you are arbitraging interest rate using theirno-interest accounts, you might get your account blocked or your profit removed. Unfortunately, such brokers are often unregulated and can do almost anything they want with your account. - Transaction costs (deposit/withdrawal fees) to keep funds properly distributed between two brokers can be prohibitive.

Triangular swap arbitrage at a single broker

Similar to the triangular price arbitrage, its swap counterpart can be performed within confines of a single Forex broker. This significantly reduces the execution risks, free margin requirements, and transaction costs. At the same time, unlike it is the case with the price arbitrage, the swap arbitrage is not viewed so adversely by brokers themselves.

The concept of triangular arbitrage in Forex has been popularized by Michal Kreslik and Bogdan Caramalac — they both have developed the basic tools for finding and executing triangular (or even quadrangular) swap arbitrage trades. The example of such a trade is described below.

Let's assume that the broker has the following swaps on three currency pairs:

- AUD/USD: +2.5 AUD for buying, −8 AUD for selling;

- USD/JPY: +0.6 USD for buying, −1.5 USD for selling;

- AUD/JPY: −0.5 AUD for buying, −3.0 AUD for selling.

The rates are currently quoted as:

- AUD/USD — 0.7422/0.7423;

- USD/JPY — 112.47/112.48;

- AUD/JPY — 83.48/83.49.

You buy 1 lot of AUD/USD and 0.7423 lots of USD/JPY. You are now exposed to a long position in AUD/JPY with the size of 1 lot. You need to hedge it by selling 1 lot of AUD/JPY. Now, you are in a triangular hedge lock, which should mitigate all the currency value risks.

From the swaps' perspective, you will be getting $1.85 ($A2.50 × 0.7422) for your AUD/USD Buy and $0.44 ($0.60 × 0.7423) for your USD/JPY Buy per day. You will also be paying $2.23 ($A3.00 × 0.7423) per day for your AUD/JPY Sell. Therefore, your total daily gain from this arbitrage setup is $0.06.

While it does not look much, it can be considered

Advantages

- Low execution risk as everything is done within one broker, and the currency rates do not matter much here (except for proper position sizing) while swaps rarely change in a matter of seconds.

- Brokers do not care much about this sort of arbitrage. Swap arbitrageurs pay good spreads and rarely see realized profit (see Disadvantages below).

Long-term passive income in case of a successful setup.- No losses due to transfer/deposit/withdrawal fees — everything is executed at one Forex broker.

Disadvantages

- Spreads — you have to recover the value lost to spreads on three trades to get to breakeven. In the above example, the total loss due to the spreads is $25.49 ($10 for AUD/USD, $6.60 for USD/JPY, and $8.89 for AUD/JPY). It would take 425 days just to recover the spread loss! Likely, the swaps would change during the period.

- Technical difficulties for coding proper opportunity detection and execution tools.

- An arbitrageur would need to hold enough margin for three (or more) positions as hedged margin reductions do not apply to indirect position locking.

Conclusion

Four methods of arbitraging the retail foreign exchange market have been described. As you can see, none of them is completely

The list does not include all the possible methods of arbitrage in currency trading. It omits a subset of techniques provided by combining spot FX with options, futures, or other trading instruments.

If you want to tell us more about how you use arbitrage opportunities in Forex, please feel free to join discussions on our forum.