The relationship between immigration and foreign exchange markets represents one of the more nuanced intersections of human movement and global finance. While discussions of Forex typically center on central bank policies, interest rate differentials, and macroeconomic indicators, the flow of people across borders exerts its own quiet but substantial influence on currency valuations, trading volumes, and the structure of the retail Forex industry itself.

This guide explores how immigration shapes exchange rates through direct monetary flows and broader economic participation, while also examining the unique ways immigrants engage with Forex markets — both as sources of currency demand and as traders navigating a globalized financial landscape.

How immigration influences exchange rates

The remittance channel: A constant flow of currency demand

Perhaps, the most direct mechanism through which immigration affects Forex markets is the remittance channel. When workers migrate to higher-income countries, they typically send a portion of their earnings back to family members in their countries of origin. These transfers, while individually modest, aggregate into staggering sums at the global level.

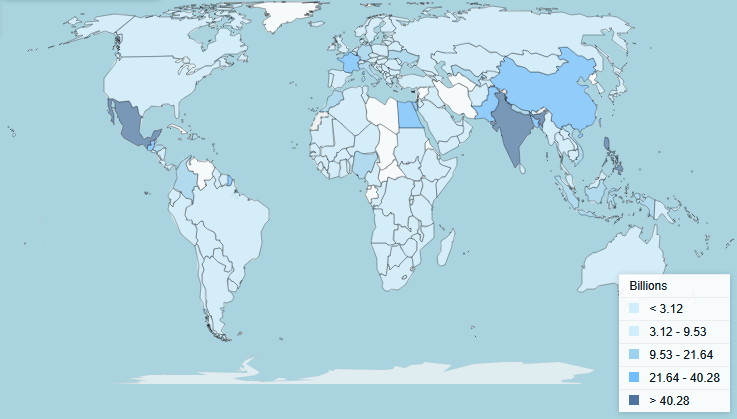

The World Bank estimates that global remittance flows to low- and middle-income countries exceed $650 billion annually, a figure that dwarfs official development assistance and rivals foreign direct investment in many regions. For certain countries, remittances constitute a substantial share of GDP — often exceeding 20% in nations like Tonga, Lebanon, Tajikistan, and Nepal.

These flows create persistent demand for the currencies of recipient countries. A Mexican worker in Texas converting dollars to pesos, a Filipino nurse in London exchanging pounds for Philippine pesos, or an Indian software engineer in Silicon Valley sending dollars home — each transaction represents a small push on exchange rates that, multiplied millions of times daily, can influence currency valuations.

The effect is particularly pronounced for smaller economies. When remittance flows are large relative to a country's foreign exchange reserves or trade volumes, they can meaningfully support the local currency. Countries experiencing diaspora growth often see their currencies stabilize or appreciate against what pure trade fundamentals might suggest, as the steady inflow of foreign currency provides a buffer against current account deficits.

Conversely, disruptions to remittance flows — whether from economic downturns in host countries, policy changes affecting immigrant workers, or global crises — can trigger currency weakness in recipient nations. The COVID-19 pandemic illustrated this dynamic clearly: initial fears of remittance collapse prompted concerns about currency stability in remittance-dependent economies, though flows proved more resilient than expected as migrants prioritized supporting families through the crisis.

The Wrold Bank map below shows the global remittance flow:

Expatriates and high-net-worth migrants: A different currency footprint

While remittances from working-class immigrants draw significant attention, wealthy expatriates and high-net-worth migrants create distinct patterns of currency demand and capital flows. Corporate executives on international assignments, entrepreneurs establishing businesses abroad, and affluent retirees relocating to favorable climates all interact with Forex markets differently than remittance-sending workers.

Expatriates typically maintain more complex multi-currency financial lives. A senior executive relocated from New York to Singapore might hold mortgage obligations in dollars, receive salary in Singapore dollars, maintain investment accounts in multiple currencies, and plan for eventual repatriation or onward relocation. These individuals often require sophisticated currency management strategies, utilizing forward contracts, multi-currency accounts, and wealth management services that generate substantial Forex market activity.

The destinations favored by wealthy expatriates — financial centers like Singapore, Hong Kong, Dubai, and Switzerland, along with lifestyle destinations like Portugal, Spain, and various Caribbean nations — see currency implications from these populations. Real estate purchases, luxury consumption, and local investment by affluent migrants create demand for local currencies, while the global orientation of these individuals ensures continued engagement with international Forex markets.

Corporate expatriate packages often include cost-of-living adjustments and currency protection provisions, reflecting the Forex risk inherent in international assignments. The treasury operations of multinational corporations managing expatriate compensation represent a meaningful segment of corporate Forex activity, hedging currency exposures created by globally distributed workforces.

Golden visa programs and citizenship-by-investment schemes explicitly target wealthy migrants, creating capital flows that affect recipient country currencies. When Portugal's golden visa program attracted billions in real estate investment from non-EU nationals, the resulting capital inflows provided support for the euro while transforming property markets in Lisbon and Porto. Similar dynamics play out in Malta, Greece, and various Caribbean nations offering residency or citizenship in exchange for investment.

Labor markets, productivity, and long-term currency fundamentals

Beyond the direct monetary channel, immigration influences exchange rates through its effects on host country economies. The relationship is complex and operates through several mechanisms.

Immigration typically expands the labor force, potentially increasing productive capacity and GDP growth. For currencies that strengthen with economic expansion — generally those of countries with stable institutions and attractive investment environments — immigration-driven growth can support long-term appreciation. The United States dollar's persistent strength over decades, for instance, partly reflects America's ability to attract global talent and channel it into productive economic activity.

Labor market effects also influence inflation dynamics, which in turn affect monetary policy and exchange rates. Immigration can moderate wage pressures in tight labor markets, potentially allowing central banks to maintain more accommodative policies than would otherwise be prudent. This indirect effect on interest rate expectations feeds through to currency valuations, as Forex traders continuously price in anticipated monetary policy trajectories.

The composition of immigration matters as well. High-skilled immigration that augments a country's technological and innovative capacity may have different currency implications than low-skilled immigration that primarily affects sectors like agriculture, construction, or services. Countries successfully attracting entrepreneurs and innovators may see enhanced productivity growth and improved terms of trade over time, supporting currency strength.

Capital flows and investment patterns

Immigrants often maintain financial connections to their countries of origin beyond simple remittances. Wealthier immigrants may hold diversified portfolios spanning multiple countries, and their investment decisions create capital flows that affect exchange rates.

When immigrants invest in assets denominated in their new home currency — purchasing real estate, contributing to retirement accounts, or building businesses — they create demand for that currency. The well-documented immigrant contribution to real estate markets in cities like Vancouver, Sydney, London, and San Francisco represents significant capital flows that support local currencies, even as they generate domestic policy debates about housing affordability.

Conversely, immigrants may also channel investment back toward their origin countries, particularly as those economies develop and offer attractive returns. This reverse flow of capital from diaspora populations can support emerging market currencies and reduce their traditional vulnerability to sudden stops in foreign investment.

The psychology of markets and immigration narratives

Currency markets respond not only to fundamental flows but also to narratives and expectations. Immigration policy debates, border developments, and demographic projections can all influence trader sentiment and currency positioning.

When markets perceive immigration policy changes as likely to affect economic growth, labor market dynamics, or fiscal balances, currencies may move in anticipation. Brexit provides a telling example: concerns about reduced access to European labor markets contributed to sterling weakness, as traders priced in potential productivity and growth implications of more restrictive immigration regimes.

Similarly, political developments perceived as immigration-restrictive or immigration-friendly in major economies can trigger Forex market reactions, particularly when traders view human capital as a key competitive advantage or vulnerability for the country in question.

Immigrants as Forex market participants

The retail Forex industry operates in a regulatory patchwork, with dramatically different rules governing leverage limits, trader protections, broker licensing, and taxation across jurisdictions. This creates an interesting dynamic for immigrants, who may maintain relationships with financial service providers in their origin countries while residing in jurisdictions with different regulatory frameworks.

An immigrant from a country with permissive Forex regulations — allowing high leverage, diverse trading instruments, and minimal restrictions — might continue trading through a broker from their home country even after relocating to a jurisdiction with stricter consumer protection rules. This is not necessarily regulatory arbitrage in a problematic sense; it may simply reflect established banking relationships, language preferences, or familiarity with specific platforms.

Consider a trader from Southeast Asia who has spent years building expertise with a broker regulated in their home jurisdiction, relocates to the European Union for employment, and wishes to continue trading. EU regulations under ESMA impose strict leverage limits (1:30 for major currency pairs, lower for others) and mandate negative balance protection. The trader's home country broker might offer 1:500 leverage and different account structures. The immigrant trader must navigate questions of residency requirements, broker compliance with EU rules, and the practicality of maintaining accounts across jurisdictions.

This dynamic creates complexity for both traders and brokers. Many international Forex brokers now maintain multiple regulated entities — one serving EU clients, another serving Asian clients, a third serving offshore clients — precisely because their customer base spans jurisdictions with incompatible regulatory requirements. Immigrant populations, with their cross-border identities and relationships, exemplify the challenges of applying nationally-bounded financial regulation to an inherently global market.

The VPN question: Technical workarounds and their risks

The tension between maintaining existing broker relationships and complying with jurisdictional requirements has led some immigrant traders to consider technical workarounds — most commonly, using Virtual Private Networks (VPNs) to mask their actual location and continue trading through brokers that might otherwise restrict or relocate their accounts.

This practice carries substantial risks that traders should carefully consider. Many brokers actively monitor for VPN usage and location discrepancies through IP analysis, device fingerprinting, and behavioral patterns. When brokers detect that a client appears to be trading from a jurisdiction different from their registered address, the consequences can be significant.

Brokers may freeze accounts pending verification of the trader's actual residence, force migration of the account to a different regulatory entity (often with less favorable conditions), close accounts entirely with limited recourse for the trader, or withhold withdrawals during investigation periods. The terms and conditions of most Forex brokers explicitly require clients to notify them of residence changes and prohibit misrepresentation of location. Traders who use VPNs to circumvent these requirements may find themselves in breach of contract, potentially forfeiting consumer protections they might otherwise enjoy.

Beyond broker-specific risks, trading through a VPN to access services not authorized in one's jurisdiction may violate local financial regulations. An EU resident trading through an offshore broker by masking their location could face regulatory consequences in their home jurisdiction, particularly if disputes arise or the activity comes to authorities' attention.

For immigrant traders, the prudent approach typically involves notifying brokers of residence changes, understanding how the move affects account status and available services, accepting the migration to an appropriate regulatory entity if required, or finding a new broker properly licensed in the new jurisdiction if the current broker cannot accommodate the change. While this may mean accepting lower leverage or different trading conditions, it provides legal certainty and access to appropriate consumer protections.

Language, trust, and broker selection

Beyond regulatory considerations, immigrants often select Forex brokers based on language accessibility and cultural familiarity. A Chinese immigrant in Australia might prefer a broker offering Mandarin customer support and familiar payment methods like WeChat Pay or Alipay. A French immigrant in Vietnam might gravitate toward brokers with French-language platforms and customer service.

This creates market opportunities for brokers who effectively serve diaspora populations. Some brokers specifically target immigrants and expatriate communities, offering localized services while operating from various regulatory jurisdictions. The resulting market structure reflects how human migration patterns influence financial service delivery.

Trust also operates through immigrant community networks. Recommendations about which brokers to use — and which to avoid — flow through diaspora communities, social media groups, and family connections. A broker's reputation within a particular immigrant community can significantly affect its ability to attract clients from that demographic.

Forex trading income and immigration decisions

A small but noteworthy segment of the Forex world involves traders whose income derives primarily or substantially from trading, and whose immigration decisions interact with their trading activity.

Some successful Forex traders, particularly those from countries with high tax burdens, restrictive regulations, or limited economic opportunities, may consider relocating to jurisdictions offering more favorable conditions. Portugal's non-habitual resident tax regime, Dubai's zero-income-tax environment, and various Caribbean citizenship-by-investment programs have all attracted attention from location-independent traders seeking to optimize their tax situations while maintaining lifestyle quality.

The decision matrix for such traders involves weighing broker access (Can I maintain relationships with my preferred brokers from this new jurisdiction?), regulatory environment (Will local regulations affect my trading strategies?), tax treatment (How will trading income be taxed?), cost of living (How far will my trading income stretch?), lifestyle factors (Climate, safety, health care, cultural amenities), and visa and residency requirements (Can I legally establish residence as a self-employed trader?).

Countries like Estonia, with its digital nomad visa and e-residency program, explicitly court location-independent professionals including traders. Cyprus has historically attracted Forex industry participants due to its EU membership, favorable tax treatment, and concentration of Forex brokers. The United Arab Emirates draws traders seeking zero income tax and a geographically strategic location bridging time zones.

This mobility creates a competition among jurisdictions for high-net-worth individuals whose income comes from global financial markets rather than local employment. The phenomenon is small relative to overall immigration flows but illustrates how financial globalization enables new patterns of human movement.

The immigrant trader's unique perspective

Immigrants who trade Forex often bring unique perspectives shaped by their cross-border experience. Having lived through currency fluctuations firsthand — perhaps seeing savings eroded by devaluation or facing the practical challenges of converting currencies for international transfers — immigrant traders may have intuitive understanding of currency dynamics that complements technical analysis.

Someone who has experienced emerging market currency crises, capital controls, or hyperinflation develops a visceral appreciation for currency risk that textbook learning cannot fully convey. This lived experience can inform trading decisions, particularly regarding risk management and position sizing in emerging market currency pairs.

Immigrant traders may also have informational advantages regarding their origin countries. Understanding local economic conditions, political developments, and cultural factors that might escape international observers can provide edge in trading specific currency pairs. A trader from Turkey genuinely understanding domestic political dynamics might interpret news events differently than a trader relying on English-language media coverage.

The Forex industry's response to global migration

Payment systems and the remittance market

The Forex industry has evolved significantly in response to immigrant demand for cross-border money transfers. Traditional remittance providers like Western Union and MoneyGram have faced competition from fintech companies offering lower fees and better exchange rates, driven partly by immigrant entrepreneurs who experienced firsthand the pain points of existing services.

Companies like Wise (formerly TransferWise), Remitly, and WorldRemit emerged to serve immigrant communities frustrated by high fees and opaque exchange rate markups on international transfers. These companies essentially compete in the retail Forex space, offering consumers better rates than traditional providers by operating on thinner margins and leveraging technology to reduce costs.

Cryptocurrency has emerged as another alternative channel, particularly appealing to immigrants in corridors poorly served by traditional finance or subject to high fees and unfavorable exchange rates. Bitcoin and other cryptocurrencies enable peer-to-peer value transfer across borders without relying on correspondent banking relationships or traditional Forex infrastructure.

Stablecoins — cryptocurrencies pegged to fiat currencies like the US dollar — have found particular adoption in remittance corridors. A worker can convert wages to a dollar-denominated stablecoin, transfer it instantly to a family member abroad, who then converts it to local currency through a local exchange. This process can be faster and cheaper than traditional remittances, though it introduces its own complexities around cryptocurrency exchange access and volatility risk during conversion.

The adoption of cryptocurrency for remittances remains uneven, concentrated among more technologically sophisticated users and in corridors where traditional options are especially expensive or unreliable. Countries with capital controls or unstable currencies — Venezuela, Nigeria, Argentina — have seen higher cryptocurrency adoption for cross-border transfers. For immigrants from these countries, crypto literacy often predates migration and influences their approach to international money movement.

Traditional Forex and remittance providers have responded to cryptocurrency competition by improving their own services, lowering fees, and in some cases integrating cryptocurrency options into their platforms. The competitive pressure from crypto alternatives has benefited immigrant consumers even when they continue using traditional services.

The competition has benefited immigrant consumers while also affecting the broader Forex ecosystem. Improved transparency in retail currency exchange puts pressure on providers across the market, and the technology developed for remittances increasingly integrates with broader financial services.

Brokers and the multi-jurisdictional challenge

Major Forex brokers have responded to global migration patterns by developing multi-jurisdictional operating structures. A single broker group might operate entities regulated in the UK, Cyprus, Australia, and offshore jurisdictions, with each entity serving clients based on their residence and the applicable regulatory requirements.

This structure accommodates immigrant populations who may prefer dealing with a familiar brand while complying with local regulations. An immigrant moving from Australia to the UK can often transfer their account between entities within the same broker group, maintaining platform familiarity while meeting new legal or fiscal obligations.

Some brokers have also developed specific marketing approaches targeting immigrant communities, sponsoring cultural events, advertising in immigrant-focused media, and offering localized services. The result is a Forex industry that increasingly reflects the global mobility of its potential customer base.

Regulatory arbitrage and consumer protection

The interaction between immigration and Forex regulation raises important consumer protection questions. When immigrants trade through brokers regulated in their origin countries rather than their country of residence, they may lack recourse to local consumer protection mechanisms if disputes arise. A resident of the European Union trading through an offshore broker cannot access EU investor compensation schemes or regulatory enforcement if the broker fails or engages in misconduct.

Regulators have responded with increasing attention to cross-border enforcement and warnings about unregulated or offshore providers. The challenge is balancing consumer protection against the practical reality that immigrants often maintain legitimate financial relationships spanning multiple jurisdictions.

Case studies and regional patterns

The Gulf States: A remittance economy

The Gulf Cooperation Council countries — Saudi Arabia, UAE, Kuwait, Qatar, Bahrain, and Oman — offer a striking example of immigration's Forex market implications. These nations host massive expatriate populations, often exceeding native citizens in number, drawn by employment opportunities in oil, construction, and services sectors.

The resulting remittance outflows are enormous. The UAE alone sees tens of billions of dollars in annual remittance outflows to countries like India, Pakistan, the Philippines, and Egypt. These flows create persistent demand for recipient country currencies against the dollar-pegged Gulf currencies, supporting exchange rates in receiving countries and influencing the business models of exchange houses throughout the region.

The concentration of Forex and remittance services in areas like Dubai's Deira neighborhood reflects the centrality of cross-border money movement to immigrant life in the Gulf. Competition among exchange houses has driven down fees and improved rates, benefiting immigrant communities while creating a substantial financial services sector.

US-Mexico corridor: The largest single bilateral flow

The United States-Mexico remittance corridor is the largest bilateral remittance flow globally, exceeding $60 billion annually in recent years. This massive flow, representing millions of individual transactions, creates constant demand for Mexican pesos and influences exchange rate dynamics for one of the world's most actively traded emerging market currency pairs.

The peso's behavior reflects remittance flows among many other factors. Seasonal patterns in remittances — higher around holidays and special occasions — create minor but detectable effects on exchange rates. More significantly, the overall health of the US economy and employment conditions in industries employing Mexican immigrants affect the trajectory of remittance flows and, by extension, peso support.

The corridor has also driven financial innovation, with numerous fintech companies specifically targeting Mexican immigrants in the US with digital transfer services, mobile apps, and competitive exchange rates.

The European Union: Free movement and currency implications

The European Union's free movement provisions created a unique natural experiment in how unrestricted migration affects currency markets. While most EU migration occurs within the eurozone (and thus does not directly involve currency exchange), significant migration from newer EU members with their own currencies — Poland, Romania, Czech Republic, Hungary — to eurozone countries created substantial cross-border flows.

Polish złoty, Romanian leu, and other Eastern European currencies receive significant support from remittances sent by workers in Germany, UK (pre-Brexit), and other Western European countries. The European Central Bank and national central banks have studied these flows as part of understanding currency dynamics within the broader European economy.

Brexit introduced a significant disruption to these patterns, with implications for sterling, the euro, and currencies of countries whose citizens had established significant presence in the UK. The subsequent reduction in EU immigration to the UK and partial relocation of EU citizens from the UK created measurable changes in remittance flows.

Future considerations

Climate migration and currency markets

Looking forward, climate-driven migration may emerge as a significant factor in Forex markets. As rising sea levels, extreme weather events, and changing agricultural conditions force population movements, the resulting shifts in remittance patterns, labor markets, and economic activity could affect currency valuations in both sending and receiving countries.

Small island nations facing existential climate threats may see currency implications from emigration, declining economic activity, and changing remittance patterns. Meanwhile, countries that absorb climate migrants may see labor market effects with inflation and monetary policy implications.

Cryptocurrency and immigration

The growing adoption of cryptocurrency for cross-border transfers creates new dynamics in the immigration-Forex nexus. Immigrants frustrated by traditional remittance costs and foreign exchange markups increasingly use Bitcoin and stablecoins for international transfers. While this activity is challenging to measure, it potentially reduces demand for traditional currency exchange services and diverts flows from the conventional Forex ecosystem.

Stablecoins pegged to the US dollar (such as USDT) have found particular adoption in countries with volatile currencies or capital controls, offering immigrants a way to move value across borders without engaging with traditional foreign exchange markets.

Digital nomadism and distributed work

The rise of remote work during and after the COVID-19 pandemic accelerated trends toward location-independent employment. More people now earn income in one currency while residing in countries with different currencies, creating patterns of currency demand and exchange that blur traditional distinctions between immigrant workers and tourists.

Digital nomad visa programs proliferating across dozens of countries explicitly target workers who earn foreign currency income. These populations — not quite immigrants in the traditional sense but far more than tourists — create currency demand patterns that challenge traditional frameworks for understanding Forex markets.

Conclusion

The relationship between immigration and foreign exchange markets reflects the deep interconnection between human movement and financial flows in a globalized world. Immigration influences exchange rates through remittance channels, labor market effects, capital flows, and market psychology. Simultaneously, immigrants engage with Forex markets as consumers of currency exchange services, as traders navigating cross-border regulatory complexity, and sometimes as location-independent professionals optimizing their lives around the possibilities of global financial markets.

For Forex traders seeking to understand currency movements, immigration patterns represent an underappreciated factor — particularly for emerging market currencies where remittance flows constitute a significant portion of foreign currency inflows. For policymakers, the confluence of immigration and Forex highlights how human mobility creates financial interdependencies that resist simple national regulation.

As global migration continues to evolve — driven by economic opportunity, climate change, conflict, and lifestyle choices — its interaction with foreign exchange markets will remain a fascinating window into how human decisions aggregate into market movements.