It is quite striking how some traders use their

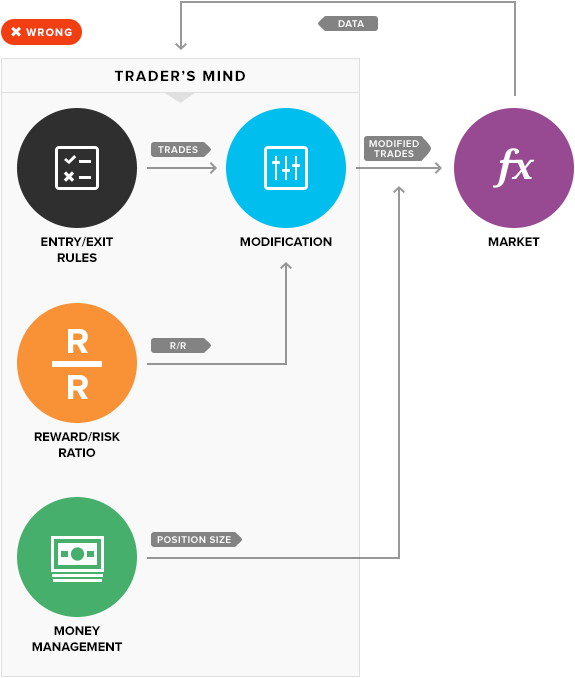

In reality, it should be the other way around. One part of a trading system should dictate the

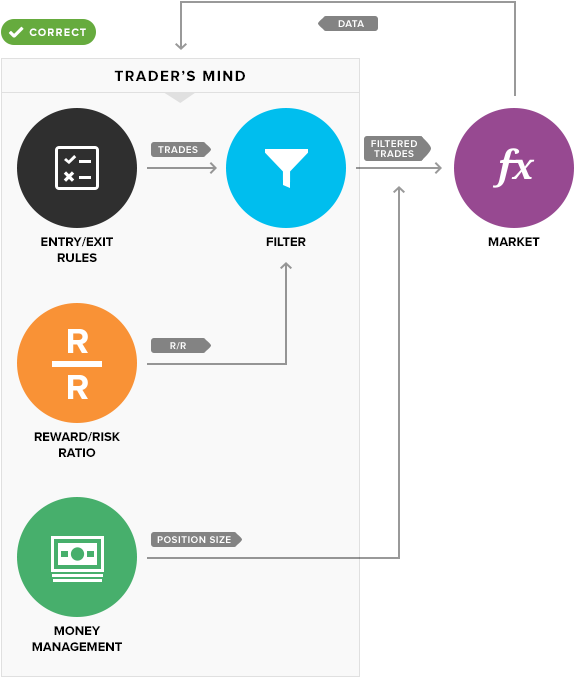

Any trader's mindset is composed of these three independent ideas:

- The idea of probability of the price reaching a certain level. This is a basic trading system idea. If you do not have it, you cannot have an edge over the market, and trading results will be just random for you. This idea is based on trader's own assumptions, experience, knowledge, skills, intuition and emotions. At any given moment it is greatly influenced by the current state of market — technical factors (price chart, indicators, trend lines, volume, etc.) and fundamental factors (news,

macro-indicators , expectations of fundamental events, etc.) Example: going long after EMA10 crosses EMA20 from below yields a higher probability for uptrend than for downtrend. - The idea of the minimum

risk-to-reward ratio (RR). It is a notion of how high RR ratio should be to justify position opening and risk taking. It is connected with the first idea in a sense that a trader may ignore signals with high enough probability if the RR is too low. Example: take trades whererisk-to-reward ratio is at least 2:1. - The idea of risk tolerance. This is how much a trader is ready to put to risk with one trade or during some period of time. It is often unrelated to a particular trading

set-up , but can depend on trader's perception of probability for the current trade (see Idea #1). Examples: 1% of account balance per trade; $100 per trade; 10% per week, etc.

A trader may have a number of any other ideas, but they will all boil down to the mentioned three when applied to actual trading process. Of course, any of these three ideas may be absent from trader's mindset, but the resulting outcomes will be unsystematic at best.

As was said earlier, the lack of the first idea leads to random trading. No risk tolerance idea leads to quick loss of the whole account balance or (in rare cases) very slow profit buildup. The lack of minimum RR ratio in a strategy is less rare and destructive but still may lead to risking too much to gain too little.

So, what does it all have to do with mixing

Here is the diagram illustrating a proper trading decision algorithm:

And this one is flawed with the RR ratio affecting position's entry and exit levels:

A kind of analogy can be drawn from binary trading. If we translate the idea of basing your entry/exit signals on your

If you have any questions or wish to express your own opinion on the validity of basing your entry and exit signals on your money management rules, feel free to start a discussion on our Forex forum.