Backtesting Strategies Based on Commitments of Traders

You can find an interesting trading system on EarnForex.com — CoT Report Trading Strategy. It is based on rigorous backtesting of 32 different trading methods that use various data from Commitments of Traders reports released by the CFTC. According to our polls, about half of Forex traders are using CoT reports in trading at least occasionally. The presented strategies offer trading opportunities based strictly on such reports. Below is a detailed description of the tools used, the backtesting process, and the results obtained.

Tools

In order to backtest anything related to the Commitments of Traders reports, it is necessary to have an expert advisor that can somehow get the data from the past history of the reports and use them to enter and exit positions. You can now download such an expert advisor for free. It is based on an MQL5 class that reads all the fields from the

The expert advisor can potentially trade any strategy based on any data from the CoT reports, but currently, it is programmed to test only 32 strategies. The spreadsheet contains the exact entry and exit signals (including additional exit signals for some strategies) for both the buy and sell sides of each of the test strategies. The following terms are used to formulate the strategies:

- Longs — long positions

- Shorts — short positions

- Dealer — Dealer / Intermediary traders

- AssetMan/Inst — Asset Managers / Institutional traders

- OI — open interest — total number of positions

- Change_in_Open_Interest_All — change in open interest of categories of traders

All changes are from a comparison to a previous weekly CoT report.

Backtesting results

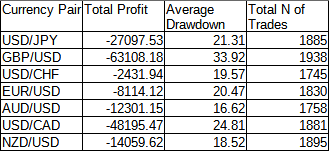

All our tests were performed on a period from January 1, 2014, to August 22, 2021, on the following currency pairs: USD/CAD, USD/CHF, GBP/USD, USD/JPY, EUR/USD, AUD/USD, and NZD/USD. A fixed position size of 0.1 standard lot was used.

The summary of the backtest results shows a table with total profit, maximum drawdown, and the number of trades for each tested strategy across each currency pair. Separate comparative tables show the total profit, the average maximum drawdown, and the total number of trades for each strategy and for each currency pair. The full set of all 224 backtesting reports with charts and complete order history are also available for downloading.

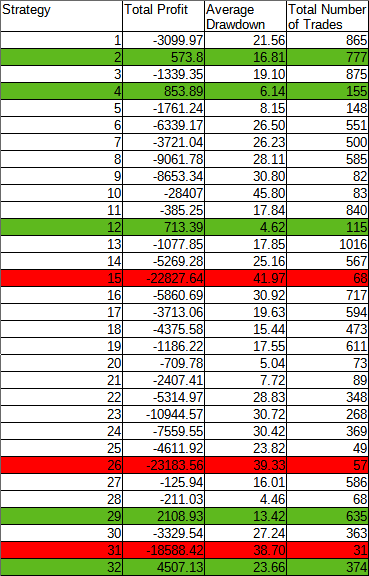

Here is the comparative table for all the tested strategies. The profitable strategies are indicated with green color, while the strategies with the biggest losses (over $15,000) are shown in red:

And here is the similar table for currency pairs:

The comparative table of results reveals the unfortunate truth that trading using the CoT report isn't as easy as taking any intuitive strategy and applying it to your favorite FX pair:

- Out of 32 strategies tested, only five showed total profit. Furthermore, all the currency pairs showed total loss when adding up the results from all the strategies.

- On top of that, even profitable strategies were highly inconsistent, often showing matching profits and losses both in number and value. For example, the strategy #32 showed the biggest total profit, yet it had losses in three out of seven currency pairs. And its largest profit of $5,214 was not that great compared with its largest loss of $3,053.

- The most consistent among the profitable strategies was the strategy #29, showing a loss in only one currency pair. Even then, profits among most currency pairs were not impressive at all.

- The most profitable combination was the strategy #32 on the GBP/USD currency pair.

- The strategies #15, #26, #31 demonstrated losses over $15,000 each. It is possible that inverting those strategies can result in profit.

- In terms of drawdown among the profitable strategies, the strategies #4 and #12 were the best, though they were rather unimpressive in terms of profit. The most profitable strategies #29 and #32 had larger drawdowns, though they were far from the worst across all the strategies.

- Among the profitable strategies, the strategy #2 and #29 executed the most trades, meaning that they were the most reliable. The strategies #2 and #12, on the other hand, had significantly fewer trades, which implies a lower reliability of their test results.

If you want to share your opinion, observations, conclusions, or simply to ask questions regarding the CoT Report Trading Strategy on Forex, feel free to join a discussion on our forum.

If you want to get news of the most recent updates to our guides or anything else related to Forex trading, you can subscribe to our monthly newsletter.